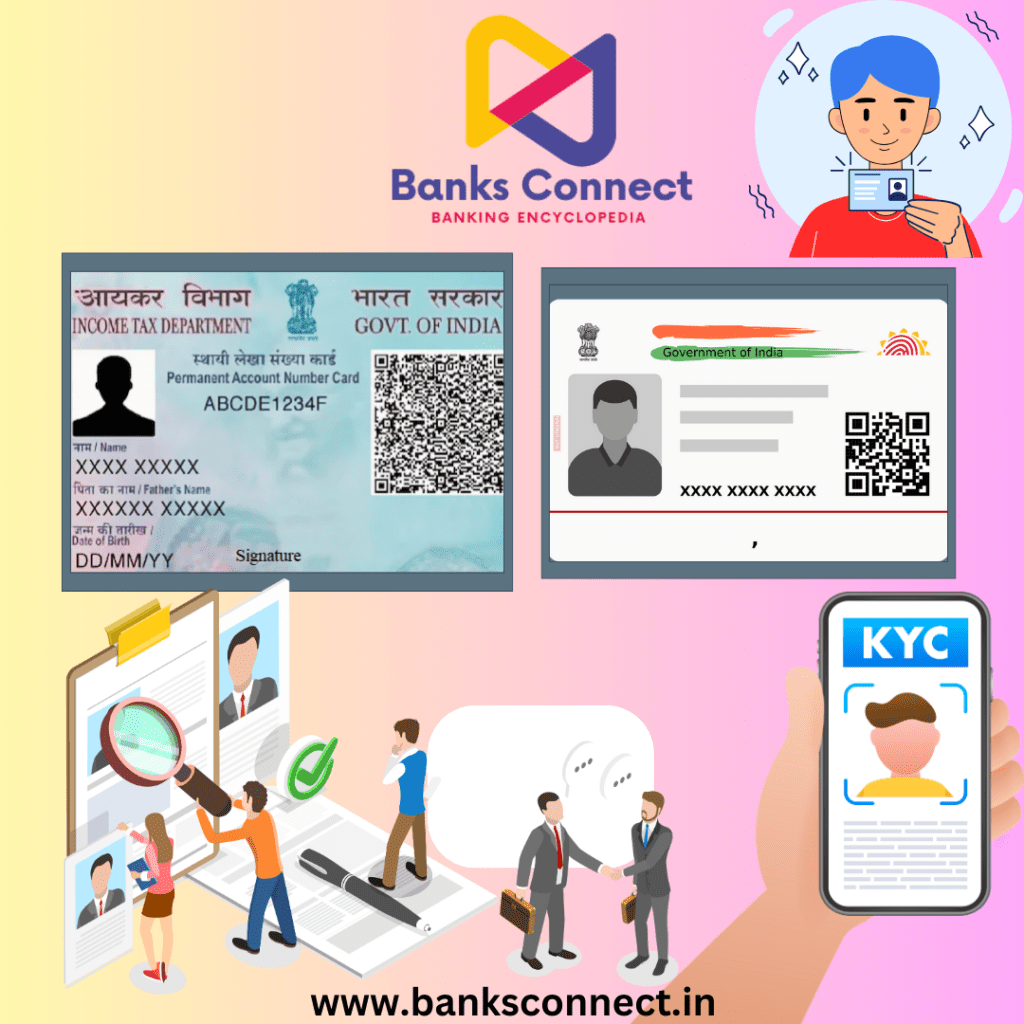

KYC, or Know Your Customer, is a vital process in the banking and financial sector. It plays a key role in verifying the identity of customers, ensuring compliance with legal requirements, and mitigating risks such as fraud and money laundering. In this guide, we’ll break down the KYC process, explain its importance, and provide actionable insights for customers.

What is KYC?

KYC is the procedure through which banks and financial institutions:

- Identify and authenticate the identity of their customers.

- Understand the financial behavior and activities of their customers.

- Monitor and mitigate risks associated with suspicious transactions, such as money laundering or terrorist financing.

Why is KYC Essential in Banking?

- Fraud Prevention

KYC helps protect banks and customers by reducing risks like identity theft and unauthorized access to accounts. - Regulatory Compliance

It ensures adherence to laws such as the Prevention of Money Laundering Act (PMLA) in India or similar regulations globally. - Transparency and Trust

By maintaining accurate customer records, banks foster transparency and build trust. - Risk Mitigation

Through KYC, banks can monitor transactions effectively, identify red flags, and ensure financial security.

Steps in the KYC Process

1. Submission of Documents

Customers need to provide valid documents for proof of identity (POI) and proof of address (POA). Examples include:

- Proof of Identity: Aadhaar card, PAN card, Passport, Voter ID, or Driver’s License.

- Proof of Address: Recent utility bills, rental agreements, or bank statements.

2. Document Verification

Banks cross-check the submitted documents with regulatory databases to verify their authenticity.

3. Risk Categorization

Customers are categorized as low, medium, or high risk based on factors like transaction patterns, location, and occupation.

4. Periodic Updates

KYC details are updated regularly, typically every two years for high-risk accounts and every ten years for low-risk accounts.

Things Customers Should Know About KYC

- KYC is Mandatory

Whether opening a new account, applying for a loan, or investing in financial products, KYC compliance is non-negotiable. - eKYC for Convenience

Many banks now offer eKYC, a hassle-free, digital process using Aadhaar-based authentication. - Consequences of Non-Compliance

Accounts that are not KYC-compliant may face restrictions, including transaction freezes. - Data Privacy

Banks are bound to protect customer data under privacy regulations, ensuring sensitive information is secure.

Example of KYC in Practice

Let’s take the case of Rahul, a young professional opening a bank account:

- Rahul submits his Aadhaar card (for POI and POA) and PAN card.

- The bank verifies his documents through Aadhaar-linked OTP authentication.

- As Rahul has a straightforward financial profile, his account is classified as low-risk.

- His savings account is opened seamlessly, and he starts transacting.

Later, Rahul updates his KYC details when he moves to a new city, submitting his updated address proof, such as a utility bill.

Benefits of KYC for Customers

- Enhanced Security

Protects customers from identity theft and unauthorized transactions. - Smooth Banking Services

Ensures uninterrupted access to accounts and banking facilities. - Simplified Onboarding

Enables easy account opening for individuals with minimal documentation via simplified KYC options.

Conclusion

The KYC process is more than just a regulatory formality—it’s the foundation of secure and transparent banking. It ensures financial institutions operate responsibly while protecting customers from fraud and financial risks. By staying compliant with KYC norms, both banks and customers contribute to a robust and trustworthy financial ecosystem.

If you’re opening a bank account or updating your records, understanding the KYC process can help you navigate it with ease. Stay informed and enjoy seamless banking services!