Why Does Your CIBIL Score Matter So Much in India?

Imagine trying to buy your dream house or your first car—your CIBIL score is the key. In India, your credit score is no less important than your physical health, especially when it comes to loans, credit cards, or even renting a home. With banks checking your financial history more often under 2025 RBI guidelines, keeping your CIBIL score healthy is essential for getting approved fast and at the best interest rates.

Understanding Different CIBIL Reports: Consumer vs. Commercial

What Is a Consumer CIBIL Report?

- Purpose: Shows the credit health of individual people (like you!).

- Covers: Personal loans, credit cards, EMI payments.

What Is a Commercial CIBIL Report?

- Purpose: Ranks the creditworthiness of businesses (like startups, partnerships, or private limited companies).

- Covers: Business loan history, company credit health.

Example: You apply for a personal loan—your consumer CIBIL score is checked. Your company applies for a business loan—it’s the commercial CIBIL report that matters!

Must-Know Credit Terms in Simple Words

What Exactly Is a CIBIL Report?

It’s your financial report card. This document details your past and present loans, credit card activity, any payment delays, and how responsibly you manage money.

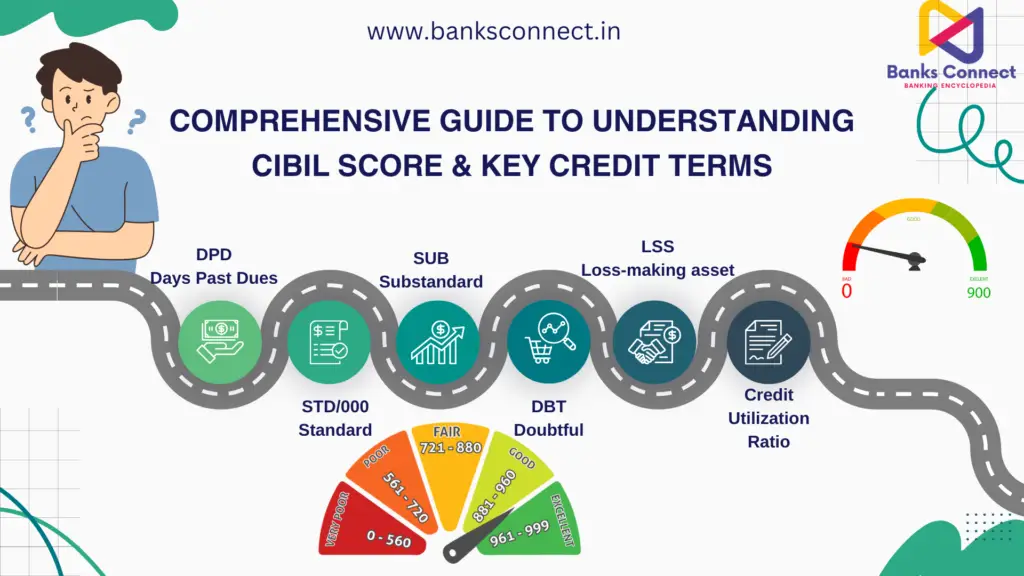

Credit Score—What’s a Good Number?

Think of your credit score as a three-digit rating (300-900). The higher, the better! For most banks in India, a CIBIL score above 750 means you’re a savvy borrower.

Credit Utilization Ratio: Why Does It Matter?

This tells lenders how much of your available credit limit you’re actually using. Try to keep it below 30% to add shine to your credit profile.

Credit Enquiries—Should You Be Worried?

Every time you apply for a loan or card, lenders ‘pull’ your CIBIL report. Too many enquiries in a short time looks risky and can make your score dip.

Default: What If You Miss a Payment?

Missing an EMI or credit card bill reduces your score, sometimes drastically. Timely payments are the easiest way to improve credit score in India.

Repayment History

Your record of paying on time (or late) is the single biggest factor affecting your CIBIL score.

Credit Mix

A blend of secured loans (like home loans) and unsecured loans (personal loans, credit cards) gives your score a positive boost.

Credit Age

How old is your oldest active loan or card? A higher credit age means experience—and that’s good in the eyes of lenders.

Credit Card Settlement

If you negotiate to pay less than you owe, your account is marked as ‘settled’—but your score will drop. Always try for a full, clean closure!

Loan Closure Status

Closed (good), Written-off (bad), Settled (not great). Banks love to see loans marked “closed” after being paid off as agreed.

DPD in CIBIL: What Do Those Codes Mean?

Your credit report often lists a “DPD value.” DPD or Days Past Due tells banks if you pay on time or not.

| DPD Value | Meaning | What It Says About You |

|---|---|---|

| XXX | No data reported | Neutral/ignored |

| 000 | Paid on time | Very positive |

| STD | Overdue ≤ 90 days | Mild risk |

| SUB | Overdue > 90 days | Risky, needs improvement |

| DBT | Overdue > 12 months | Very risky |

| LSS | Debt written off | Critical issue, avoid loans |

Tip: Only XXX and 000 on your report are truly “safe.” Avoid SUB, DBT, and especially LSS!

2025 RBI & CIBIL Updates You Need to Know

- Score updated twice a month: Actions show up quickly—good and bad!

- One free CIBIL report a year: Check yours and spot mistakes.

- Dispute errors fast: New rules get your issues resolved in 7 days.

- Transparency: Get alerts if someone checks your report.

Top Tips to Improve Your CIBIL Score in India

- Pay EMIs and credit card dues before or on the due date.

- Don’t “settle”—always fully close accounts wherever possible.

- Use less than 30% of your total card limit.

- Don’t apply for too many loans at once.

- Regularly monitor your CIBIL score and credit report.

Conclusion: Take Charge of Your Financial Health

Your CIBIL score is your ticket to affordable credit and financial freedom in India. By focusing on timely payments, avoiding negative DPD values, and monitoring your report, you’re putting your best foot forward. Need help understanding your report or boosting your score? Connect with us at BanksConnect.in—we’re here to guide you with simple, actionable financial advice!