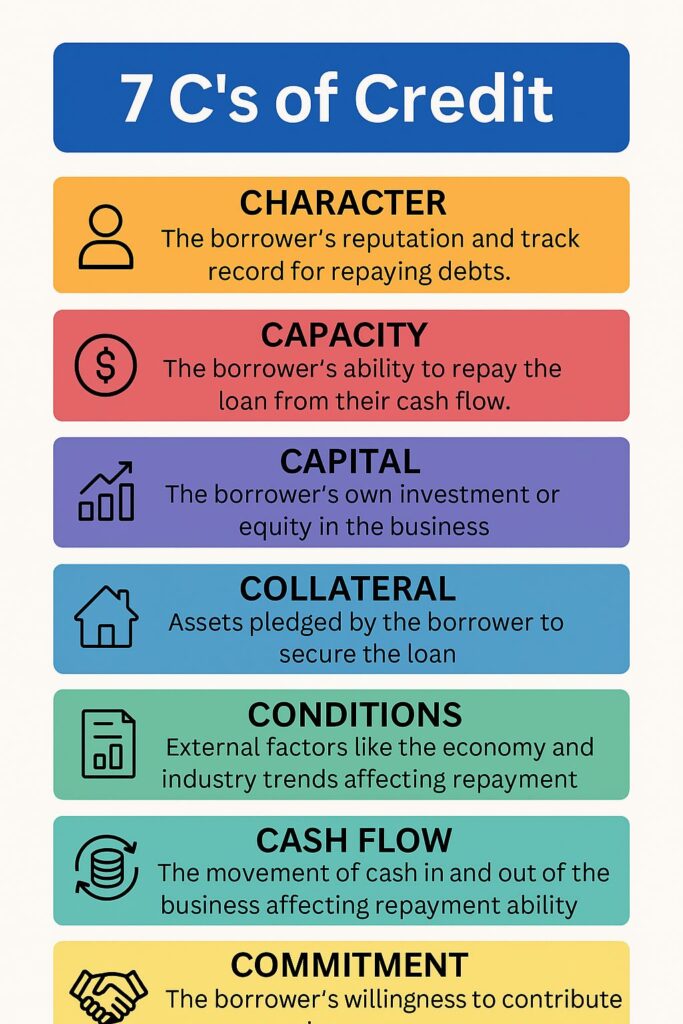

When it comes to lending, banks follow a meticulous process of credit assessment to ensure they are making informed decisions. This process is crucial for managing risk while also promoting responsible lending. The “7 C’s of Credit” framework is commonly used to evaluate the creditworthiness of borrowers. This approach helps banks determine the likelihood that a borrower will be able to repay their loan. Let’s break down the 7 C’s of Credit and how each component plays a role in credit assessment.

1. Character – Trustworthiness of the Borrower

Character is the first key factor in credit assessment. It refers to the borrower’s reputation and history of repaying debts. Lenders assess this by reviewing the borrower’s track record and overall integrity. A borrower with a strong reputation and a history of fulfilling financial obligations is considered less risky.

How Banks Assess Character:

- Credit History Reports (e.g., eCIB): These reports provide a clear view of the borrower’s past behavior when it comes to debt repayment.

- References: Banks may also consult references from suppliers, competitors, or other business partners.

- Background Checks: A comprehensive background check can reveal any potential red flags regarding the borrower’s credibility.

2. Capacity – Can the Borrower Repay the Loan?

The second “C” is Capacity, which refers to the borrower’s ability to repay the loan. This is assessed by examining the borrower’s financial health and their ability to generate sufficient income or cash flow.

Assessing Capacity:

- Financial Statements: Income statements and balance sheets reveal the borrower’s financial situation.

- Net Worth: The borrower’s personal net worth helps determine how much equity they have invested in their business or project.

- Debt Service Coverage Ratio (DSCR): This ratio measures the borrower’s ability to pay debt with their available cash flow.

- Existing Debts: Evaluating existing obligations helps determine if the borrower can handle more debt without risking financial strain.

3. Capital – Borrower’s Financial Investment

Capital represents the borrower’s own financial stake in the business or project. A borrower who has invested a significant amount of their own capital shows commitment and reduces the lender’s risk.

Why Capital is Important:

- A higher equity investment by the borrower often signals a lower likelihood of default, as the borrower has a personal financial interest in the success of the project.

4. Collateral – Securing the Loan

Collateral refers to assets offered by the borrower to secure the loan. If the borrower defaults, the bank can seize the collateral to recover its losses. This provides an added layer of security for lenders.

Types of Collateral:

- Real Estate: Property is often used as collateral for loans.

- Inventory: Businesses may pledge their inventory or products.

- Equipment: Machinery and valuable equipment can be used as collateral.

- Corporate Guarantees: In some cases, guarantees from other businesses may serve as collateral.

5. Conditions – External Factors Affecting the Borrower’s Ability to Repay

Conditions refer to the internal and external factors that might impact the borrower’s ability to repay the loan. These factors can include industry trends, the health of the economy, and the regulatory environment.

Key Condition Factors:

- Industry Health: The performance of the borrower’s industry plays a significant role in their financial outlook.

- Economic Trends: A downturn in the economy could affect the borrower’s ability to generate income.

- Regulatory Changes: Changes in regulations or laws may influence the borrower’s operations and ability to repay.

- Loan Purpose and Terms: The specific use of the loan and its terms can also impact the borrower’s repayment ability.

6. Cash Flow – A Key Indicator of Repayment Ability

Cash Flow is one of the most critical factors in assessing creditworthiness. It refers to the borrower’s actual income and expenses, and how well they manage their day-to-day financial operations.

Why Cash Flow is Essential:

- Adequacy to Service Debt: Lenders need to ensure that the borrower has enough cash flow to cover the loan repayments.

- Consistency: Banks prefer borrowers with consistent cash flow patterns, as this ensures the borrower can meet repayment obligations over time.

7. Commitment – The Borrower’s Willingness to Fulfill Loan Terms

Commitment refers to the borrower’s willingness to contribute to the loan and take on personal risk. This shows the lender that the borrower is serious about repaying the loan and making the business or project successful.

How Commitment is Evaluated:

- Personal Guarantees: A borrower who is willing to provide personal guarantees shows strong commitment.

- Equity Contribution: A larger personal investment often signifies that the borrower is highly invested in the project’s success.

Conclusion: The Importance of a Systematic Credit Assessment

The 7 C’s of Credit provide a structured approach to assessing a borrower’s creditworthiness. By examining factors such as Character, Capacity, Capital, Collateral, Conditions, Cash Flow, and Commitment, banks can make well-informed decisions when extending credit. This systematic approach helps banks reduce risk, ensure responsible lending, and maintain financial stability.

Understanding these key factors can also empower borrowers to improve their creditworthiness and increase their chances of securing loans. Whether you’re a bank or a borrower, a clear understanding of the credit assessment process is essential for building trust and fostering long-term financial relationships.