Introduction: Choosing the Right Loan for Your Financial Goals

Loans play a vital role in helping individuals and businesses achieve their dreams—whether it’s buying a home, funding education, or growing a company. But with so many loan options available, how do you pick the right one? This guide breaks down the major types of loans in India, explains their benefits and eligibility criteria, and offers simple tips to help you make smart borrowing decisions in 2025.

Secured vs. Unsecured Loans: What’s the Difference?

Secured Loans

Secured loans require collateral—a valuable asset you pledge as security. If you can’t repay, the lender may take the asset to recover their money.

Examples of secured loans:

- Home loans

- Auto loans

- Gold loans

- Loan against property

Why choose secured loans?

- Lower interest rates

- Higher loan amounts

- Longer repayment periods

Unsecured Loans

Unsecured loans don’t require collateral. Approval depends mostly on your creditworthiness.

Examples of unsecured loans:

- Personal loans

- Credit card loans

- Education loans

Benefits:

- No need to pledge assets

- Faster approval and disbursal

- Perfect for short-term or immediate needs

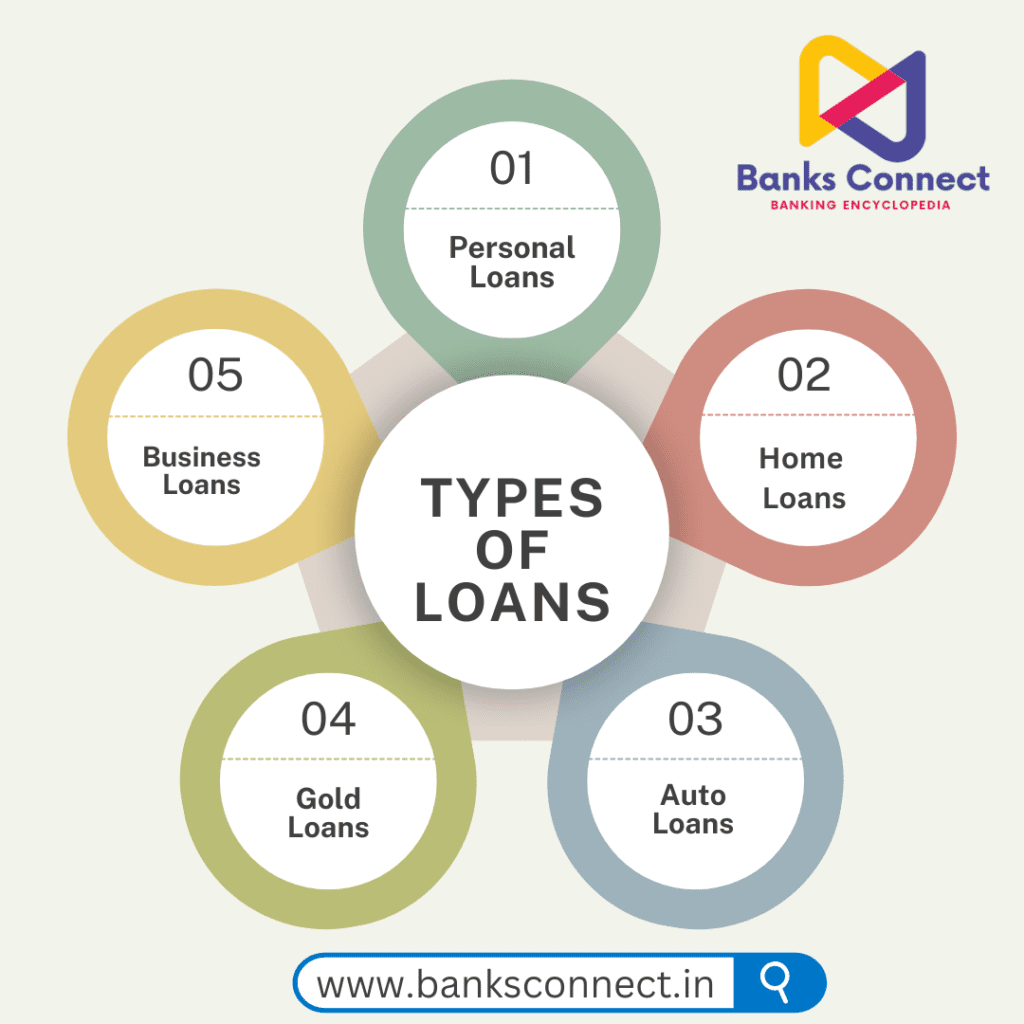

Types of Loans in India: Features, Eligibility & Real-Life Examples

1. Personal Loans: Flexible and Fast

Ideal for medical bills, weddings, or travel expenses, personal loans are unsecured but require a good credit score.

Eligibility:

- Salaried or self-employed individuals

- FOIR (Fixed Obligations to Income Ratio) under 40–50%

- Credit score preferably 750+

Example:

Ramesh earns Rs. 50,000/month and manages EMIs of Rs. 5,000. With an FOIR limit of Rs. 25,000, he can borrow Rs. 5 lakh at 12% interest for 5 years, maintaining affordable EMIs.

2. Home Loans: Your Path to Real Estate Ownership

Home loans are secured and help you purchase or build your dream home.

Eligibility:

- Stable income for salaried or self-employed

- Banks finance 75–90% of property value

- Repayment capacity based on income and liabilities

Example:

Priya plans to buy a house worth Rs. 50 lakh. The bank finances 80% (Rs. 40 lakh) at 7% interest over 20 years, resulting in an EMI of about Rs. 31,000.

3. Auto Loans: Drive Your Dream Car

These loans help finance new or used vehicle purchases with attractive rates and tenure.

Eligibility:

- Salaried individuals, professionals, or businesses

- Loan up to 70–90% of vehicle price

- Good credit score is essential

Example:

Ajay gets an auto loan for Rs. 8.5 lakh on a Rs. 10 lakh car at 9% interest for 5 years, with monthly EMIs around Rs. 17,600.

4. Education Loans: Investing in Your Future

Education loans cover higher studies in India or abroad, sometimes requiring collateral for larger amounts.

Eligibility:

- Students with parents or guardians as co-borrowers

- Loans up to Rs. 7.5 lakh usually collateral-free

Example:

Ananya secures Rs. 15 lakh for her MBA course with her father as co-borrower, with repayments starting six months after graduation.

5. Gold Loans: Quick Cash Using Your Jewelry

Gold loans are quick, hassle-free loans secured by pledging gold ornaments.

Eligibility:

- Loan up to 75–90% of gold’s value

- Minimal documentation

Example:

Sunita pledges gold worth Rs. 5 lakh and gets Rs. 4 lakh loan repayable in 6 months at 10% interest.

6. Business Loans: Fueling Your Growth

Supporting SMEs and established businesses, business loans finance expansion, equipment, or working capital.

Eligibility:

- Based on turnover, profitability, and financial statements

Example:

Raj’s SME with Rs. 1 crore turnover gets Rs. 20 lakh working capital loan at 12% interest.

7. Agricultural Loans: Supporting India’s Farmers

These loans help farmers buy equipment, seeds, or irrigation systems with government subsidies often available.

Eligibility:

- Based on landholding and crop type

- Subsidized rates via schemes like Kisan Credit Card

Example:

A farmer borrows Rs. 2 lakh under Kisan Credit Card scheme at subsidized 4% interest to buy a tractor.

Loan Comparison Table

| Loan Type | Secured? | Ideal For | Collateral | Max Tenure | Interest Rate Range |

|---|---|---|---|---|---|

| Personal Loan | No | Emergencies, personal expenses | No | 5 Years | 10% – 24% |

| Home Loan | Yes | Property purchase | Yes | 30 Years | 6% – 10% |

| Auto Loan | Yes | Vehicle purchase | Yes | 7 Years | 8% – 12% |

| Education Loan | Maybe | Higher education | Maybe | 15 Years | 8% – 13% |

| Gold Loan | Yes | Short-term cash needs | Yes | 1-2 Years | 9% – 14% |

| Business Loan | Maybe | SMEs and business needs | Maybe | 5-15 Years | 10% – 18% |

| Agricultural Loan | Yes | Farming and equipment purchase | Yes | Varies | 4% – 10% (subsidized) |

Key Tips Before You Take a Loan

- Assess Your Needs: Borrow only what you truly need and can repay comfortably.

- Know Your Loan Type: Match loan type to your financial goals.

- Check Your Credit Score: Higher scores unlock better interest rates.

- Compare Offers: Rates, fees, and terms vary—shop around.

- Read the Fine Print: Watch for hidden charges and prepayment penalties.

- Calculate EMI Carefully: Ensure monthly payments fit your budget without strain.

Fair Practices for Borrowers and Lenders

For Borrowers:

- Be honest on loan applications

- Repay EMIs timely

- Disclose all current liabilities

For Lenders:

- Provide clear, transparent loan terms

- Maintain borrower confidentiality

- Follow ethical recovery processes

Frequently Asked Questions (FAQs)

Q: What is the difference between secured and unsecured loans?

A: Secured loans require collateral, offering lower interest rates, while unsecured loans don’t but typically carry higher rates.

Q: What is FOIR and why does it matter?

A: FOIR (Fixed Obligations to Income Ratio) shows the percentage of your income committed to EMIs, helping lenders assess your repayment capacity.

Q: Can I get a loan with a low credit score?

A: It’s possible but likely at higher interest rates and with stricter terms.

Q: Should I choose a personal loan or use a credit card for expenses?

A: For large, longer-term needs, personal loans are better; credit cards suit smaller, short-term needs if paid on time.

Q: What are prepayment and foreclosure charges?

A: These are fees charged if you repay the loan before the tenure ends. Always check these charges beforehand.

Conclusion: Borrow Smart, Grow Financially

Choosing the right loan isn’t just about borrowing money—it’s about understanding your financial goals and picking an option that supports your journey. With clear knowledge of loan types, eligibility, and repayment, you can steer your finances confidently in 2025 and beyond.

Need help comparing loans or checking your eligibility? Connect with us at BanksConnect.in — your trusted partner in smart financial decisions.